New Zealand Credit Risk and Fraud Summit insights series – by Jordan Harris, Director of Product, Open Data Solutions, Experian

At this year’s New Zealand Credit Risk and Fraud Summit, I led a roundtable discussion with senior risk and fraud leaders on the potential transaction data has to contribute to credit risk and fraud as New Zealand’s open data environment develops.

Consumer Data Right (CDR) will create a more standardised route to permissioned transaction data in New Zealand. As access becomes more consistent, organisations may increasingly differentiate through how well they interpret, govern and apply the data.

Experian has spent more than a decade helping organisations collect, enrich and apply transaction data across personal financial management, digital banking, lending, affordability assessment, credit risk and fraud. The roundtable drew on that experience to explore three practical questions for New Zealand organisations: how to build strong transaction-data foundations, where transaction data can support risk and fraud outcomes, and what to watch out for as more organisations begin using permissioned data.

CDR is widening access to permissioned transaction data

Many consumers in New Zealand manage their financial lives across more than one provider. A lender may see part of a consumer’s financial activity internally, while income, recurring commitments or early signs of financial pressure may appear in accounts held elsewhere.

As CDR adoption develops, risk and fraud teams will have a more consistent way to request and use permissioned transaction data from external accounts. Each organisation will still need to decide how that information should sit alongside the data it already uses, including bureau information, internal account history, application data and applicant-supplied evidence.

The useful question is where that external account activity can improve an existing assessment or treatment. In affordability assessment, it may help clarify income and commitments. In fraud review, it may help assess whether application claims align with observed account behaviour. In account management or collections, it may help teams understand whether a consumer’s financial position appears to be changing.

Strong transaction enrichment as the foundation

Experian’s decade of transaction-data work has shown that the quality of the transaction data enrichment shapes how reliably the data can be used across credit risk, fraud and affordability. Raw transaction records capture real behaviour, but variables such as payroll references, merchant descriptors, transfers and repayment activity often need interpretation before they can support specific use cases.

Transaction enrichment can be used to recognise recurring income, standardise merchant names, identify regular commitments, distinguish discretionary spend from obligations, and help surface patterns such as buffers, volatility or potential financial stress.

The context for the data interpretation can also change based on the use case: personal financial management may only need broader spending categories, while credit risk, fraud and affordability processes often require more detailed merchant resolution, income recognition and commitment detection.

Weak categorisation can create downstream cost and complexity once it is embedded in rules, scores or workflows. Teams may have to manage unclear income, merchant or commitment interpretation through manual review, exception rules or model adjustments that could have been reduced with stronger enrichment earlier.

We have recently launched a new transaction enrichment solution for New Zealand - Experian Money Tracker.

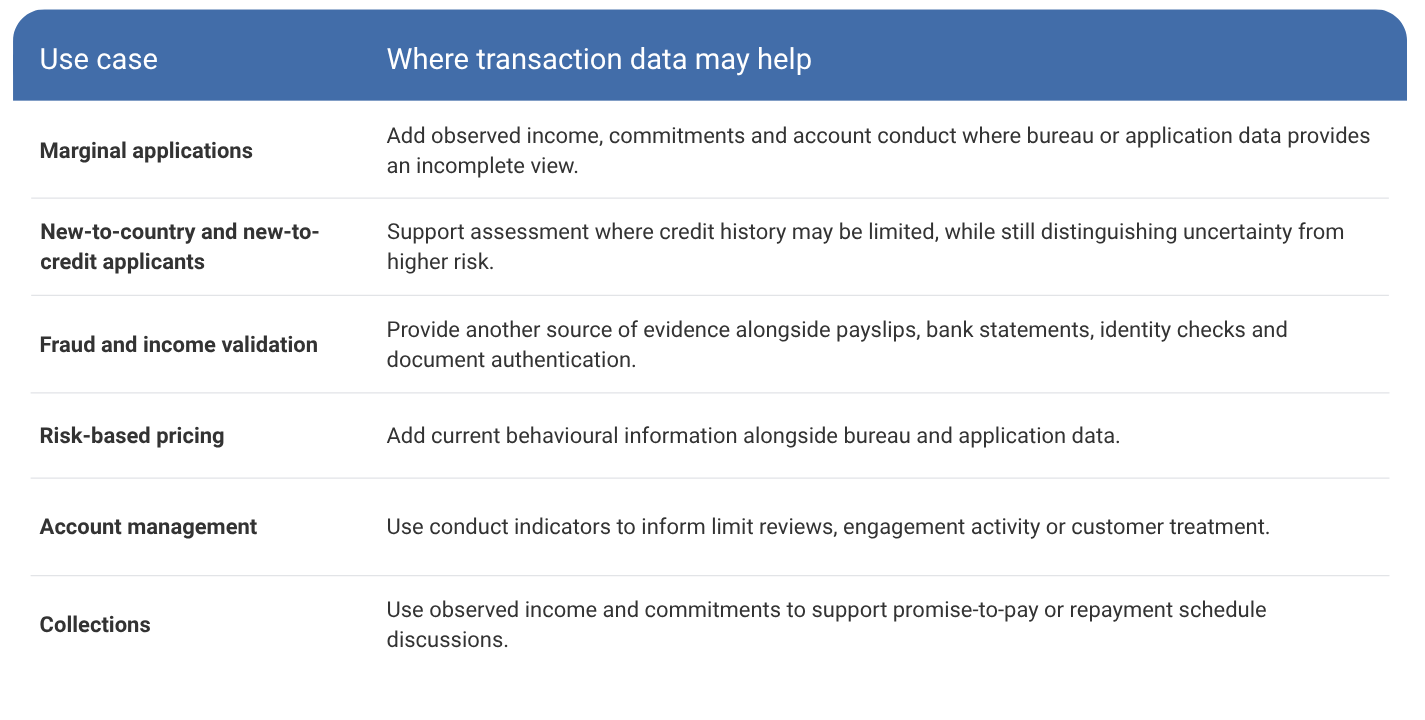

Use cases extend across the lifecycle

Transaction data is often first considered for onboarding or affordability, although the roundtable explored applications across origination, fraud, pricing, account management and collections:

Implementation watch-outs

The roundtable also covered implementation choices that can reduce the usefulness of transaction data.

Building rules, scores or workflows directly on raw transaction narratives can create unstable foundations, while relying too heavily on predictive matching for foundational enrichment can mask uncertainty in the underlying categorisation.

Transaction data can also become another source of complexity if it is added to an existing underwriting or review flow without changing the way the process works. The more useful exercise is to decide what the additional behavioural evidence should change: when further information is requested, where friction is justified, when review is triggered and how the result is measured.

Ultimately, business buy-in can be a challenge when transaction data is positioned mainly as a risk-detection tool. Transaction data initiatives are more likely to gain support when they also show how transaction data may help reduce unnecessary customer experience friction, support marginal assessments, inform fraud controls or improve customer support conversations.

Key takeaways for New Zealand organisations

For organisations preparing for broader use of permissioned transaction data, three priorities stand out:

- First, define where transaction data should improve the process, whether that is affordability assessment, fraud review, marginal application assessment, pricing, account management or collections treatment.

- Second, investment in transaction enrichment capability should be considered a foundation. Merchant identification, income recognition, spending categorisation and commitment detection need to be reliable enough for the decision or process being supported.

- Finally, tap into prior experience. As open data adoption continues to devleop in New Zealand, the opportunity is to apply lessons already learned from transaction-data work and build the capability to enrich, govern and apply permissioned data with purpose.

To find out how Experian is supporting organisations with open data, transaction enrichment and decisioning, please get in contact through the form below.