Accuracy and speed – the fundamental requirements for creditworthiness assessment. And in a competitive financial environment, the need for fast and highly precise decisions are key differentiators. Yet achieving these goals remains a significant challenge for many organisations.

Why is that? The biggest challenge is that credit risk management is often a complex web of processes, with data preparation, model development and credit decisioning happening in disconnected systems. This often results in a laborious, time-consuming and convoluted series of processes.

Experian’s latest research shows the number one pain point when it comes to credit risk models is the time it takes to develop, update, and push new models into production. The ability to develop and deploy models quickly has become critical to adapt to changing regulatory and macroeconomic conditions.

The solution to this pain point is greater connectivity and integration of data, Model Ops and decisioning software into a single cloud-based platform. This article provides a summary of our latest report: From Data to Decision: Discussions on a Unified Platform. Click on the link below to access your complimentary copy of the full report.

From Data to Decision: Discussions on a Unified Platform

DownloadWhat is a unified credit and fraud platform?

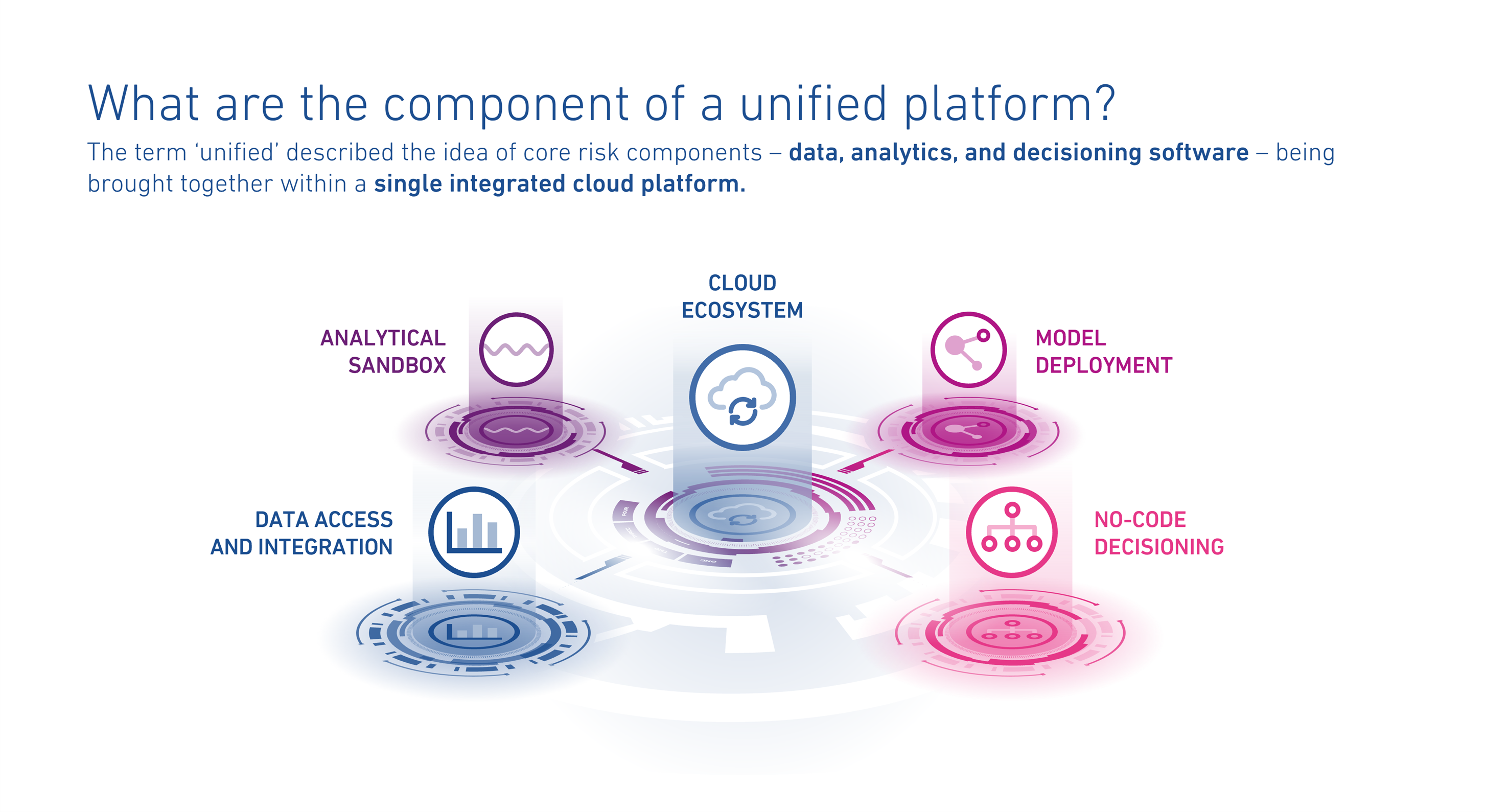

The journey from data to decision is a complex process that connects different datasets, software and business units. Breaking this process down into its core building blocks is necessary for a high-level viewpoint and to provide an understanding of how each block is connected.

From this perspective, it is easier to see how greater integration between blocks allows for a more streamlined process that ultimately results in faster model lifecycles and more accurate credit risk management and fraud decisions.

Underlying each of these blocks is the bedrock of cloud – this is the critical foundation that enables interoperability between the following blocks:

- Block 1 – Data access and integration

- Block 2 – Analytical Sandbox

- Block 3 – Model deployment

- Block 4 – No code decisioning

Understanding the components of a unified platform

Let’s take a closer look at each building block to explore how a unified platform can improve efficiency. In the full report we discuss the core needs associated with each block in detail.

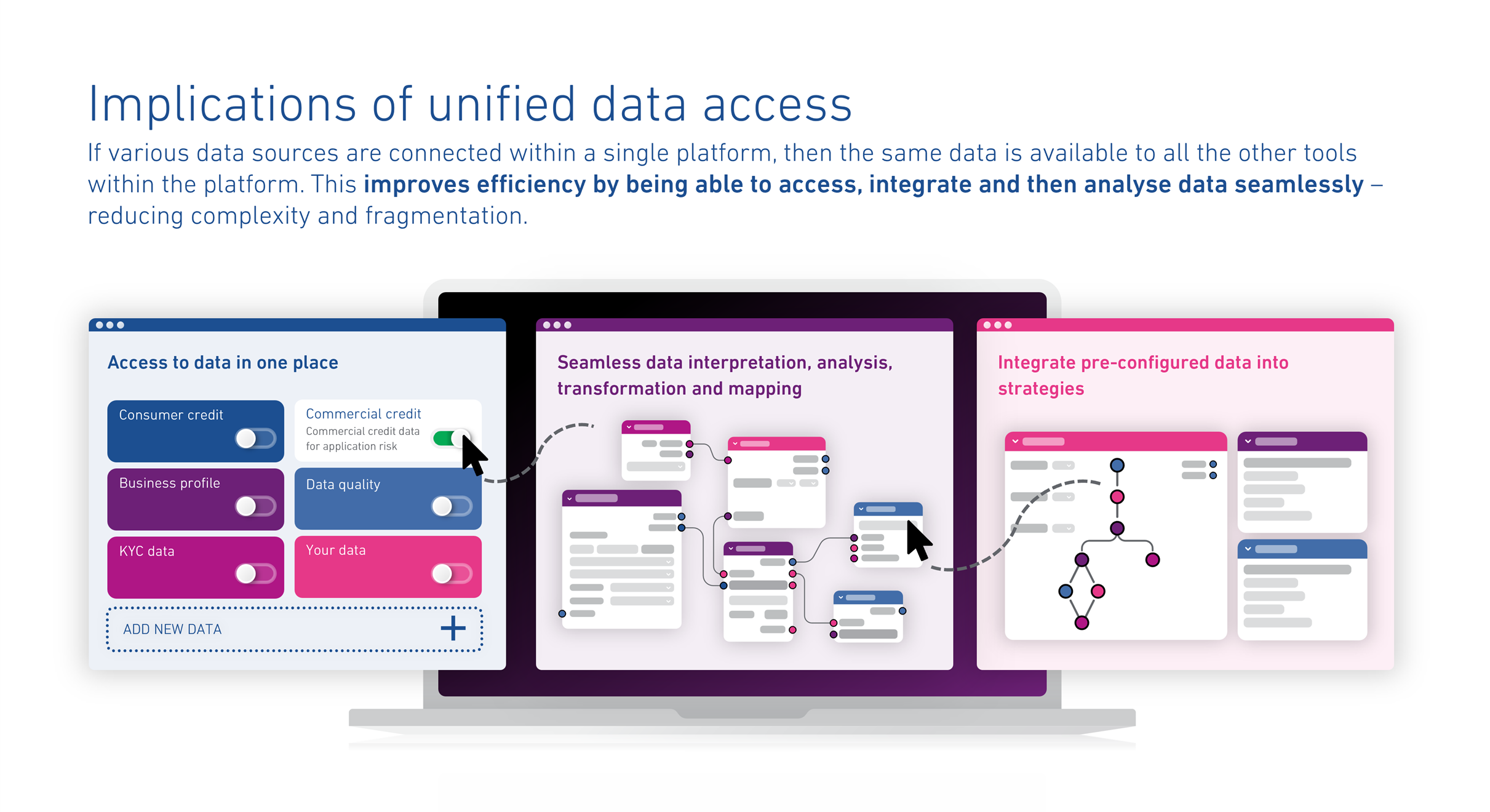

Block 1 – Data access and integration

The volume of available data is growing exponentially. And as the number of data sources used for credit and fraud decisions increases, how different units within an organisation access it has become increasingly important.

Cloud provides the elastic infrastructure needed to optimise data storage and APIs make it possible to connect data to systems in faster ways. For a unified platform to work, simplified data access and connectivity between applications is vital.

Block 2 – Analytical sandbox

By connecting an analytical sandbox with all the relevant datasets on a unified platform, businesses can make sense of disconnected data. It allows a variety of structured and unstructured databases to be consolidated into a single environment, where they can be normalised, cleansed and prepared for analysis – simplifying data governance and security.

With a range of analytical tools available in the sandbox, different users can simultaneously and collaboratively experiment with different types of model development – in a safe environment. Once models are developed and tested in the sandbox, they can be seamlessly transferred to the model deployment stage.

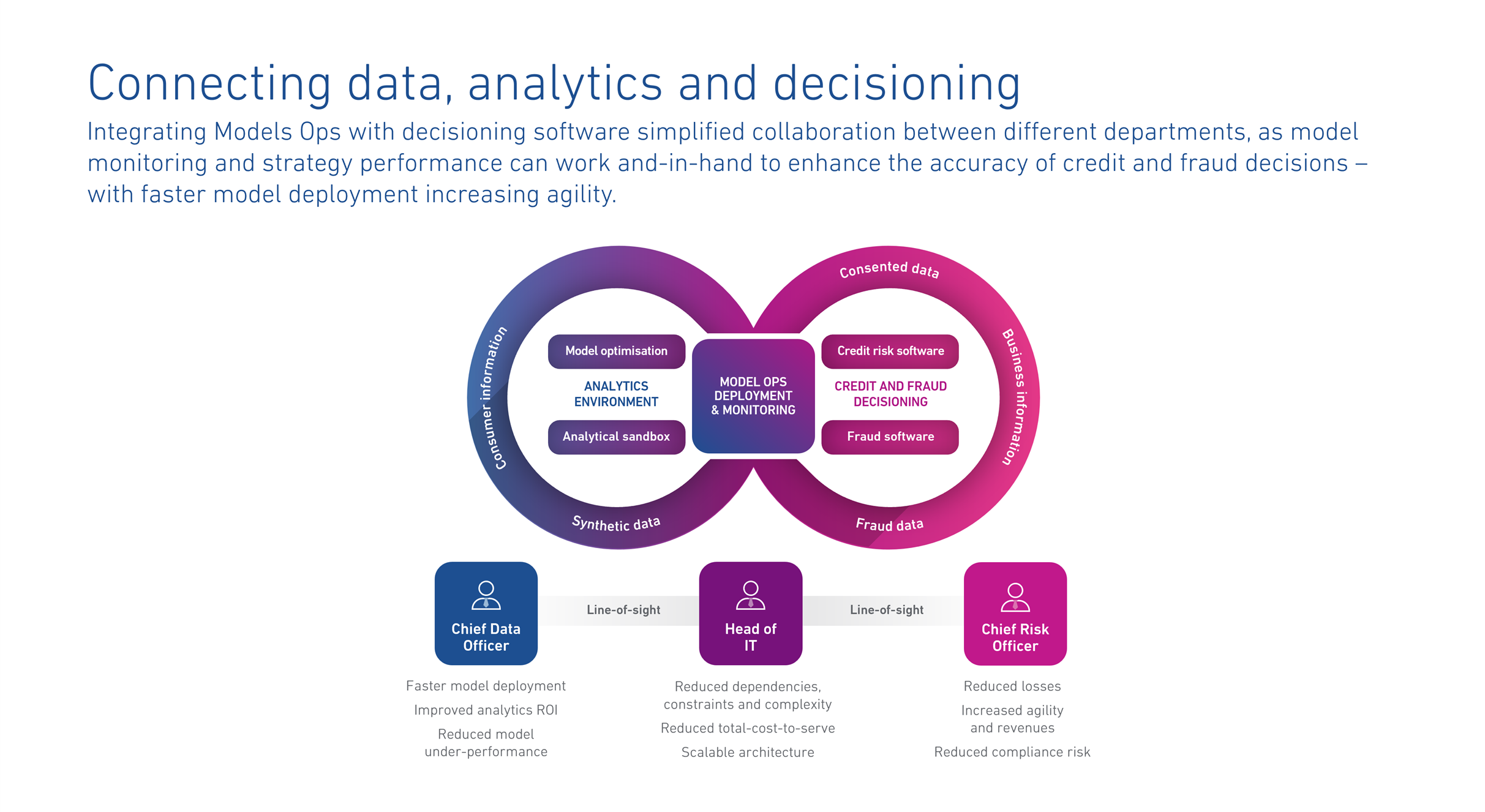

Block 3 – Model deployment

The longer it takes to get a model live, the more delayed its impact is, which reduces the return on investment. Considering that close to half (48%) of businesses are updating models more frequently than ever before, a slow deployment process can have a noticeable impact profitability.

A unified platform can reduce the time required for model deployment by eliminating the need for IT teams to re-code models before moving them into production. This direct integration between Model Ops and decisioning software streamlines the back-and-forth between data preparation, model engineering, deployment and monitoring, which often cause significant delays.

Block 4 – No code decisioning

Simple to use, drag-and-drop interfaces are now built into modern credit and fraud decisioning software. By building functionality that requires no coding, this type of interface empowers a wider range of business users to create and manage both simple and complex decisions. This reduces reliance on advanced technical experts.

This type of user interface allows lenders to design strategies that take advantage of the increased predictive accuracy of Machine Learning (ML) models. The software should allow ML models to be tested and simulated to understand the impact on performance prior to deployment.

Block 5 – Cloud ecosystem

Cloud infrastructure is the essential substructure underpinning a unified risk and fraud platform. It is necessary because it allows for a diverse range of datasets and software tools to be fully integrated.

For example, a credit originations journey involves many processes that must be stitched together – affordability assessments, risk modelling, testing, identity verification, fraud checks, and decision workflows. This process often involves a combination of in-house systems and third-party systems, involving different databases and platforms.

It is only with a cloud platform that these different components can be brought together in a way that ensures a highly secure and seamless connection between them.

From Data to Decision: Discussions on a Unified Platform

DownloadKey benefits that a unified platform has on credit risk and fraud management

One of the biggest benefits of a unified platform is that all the relevant applications are in one place and are accessible to users via a single sign-on. Users can select the relevant application for their task but also switch seamlessly between other applications and services.

A unified approach helps improve user experience by making it easier to move between applications. It allows businesses to build a model in the sandbox environment, then auto-register in the Model Ops application with the necessary regression testing and compliance checks, approve them, and then pull those models (and the supporting documentation) immediately into the decisioning software ready for action.

In the past, this process would involve hopping between different services and vendors, but with a unified platform, the process is more ergonomic and streamlined.

The benefit of this approach is that it allows for more effective overall risk management, improves operational efficiency, and reduces costs.

How? By empowering different users to accelerate and scale their specific activities. This allows more models to be deployed and improves productivity and collaboration, which can significantly improve the accuracy of credit risk and fraud decisions.

Are you interested in finding out more about Experian’s unified platform?

The short video below discusses how the Experian Ascend Platform integrates all the data and software tools required for automated credit risk management and fraud prevention in a seamless way.

If you would like to explore a detailed analysis of the necessary requirements involved with a unified platform and the advantages of this approach, simply click on the link below to access your copy of our analyst report.

From Data to Decision: Discussions on a Unified Platform

DownloadContact us to speak to an expert and elevate your credit risk management and fraud prevention today.

© Experian, 2026. All rights reserved. The word “EXPERIAN” and the graphical device are trademarks of Experian or its related bodies corporate and may be registered in the EU, USA and other countries. The graphical device is a registered Community design in the EU. Other product and company names mentioned herein are the trademarks of their respective owners.

Disclaimer: This blog is provided by Experian Australia Pty Ltd (“Experian”) as general information and it is not (and does not contain any form of) professional, legal or financial advice. Experian and its related bodies corporate make no representations, warranties or guarantees that the information (including links and the views/opinions of authors and/or contributors) contained in this blog are error free, accurate or complete. You are solely responsible and liable for any decision made (or not made) by you in connection with the information contained in this blog. Experian (and its related bodies corporate) exclude all liability for any and all loss cost, expense, damage or claim incurred by a party as a result of or in connection with (whether directly or indirectly) this blog or any reliance on the information in this blog or links contained within. Experian owns (or has appropriate licences for) all intellectual property rights in the information and this blog must not be edited, copied, updated or republished (whether in whole or in part) in any way without Experian’s prior written consent.