Why time to market defines impact

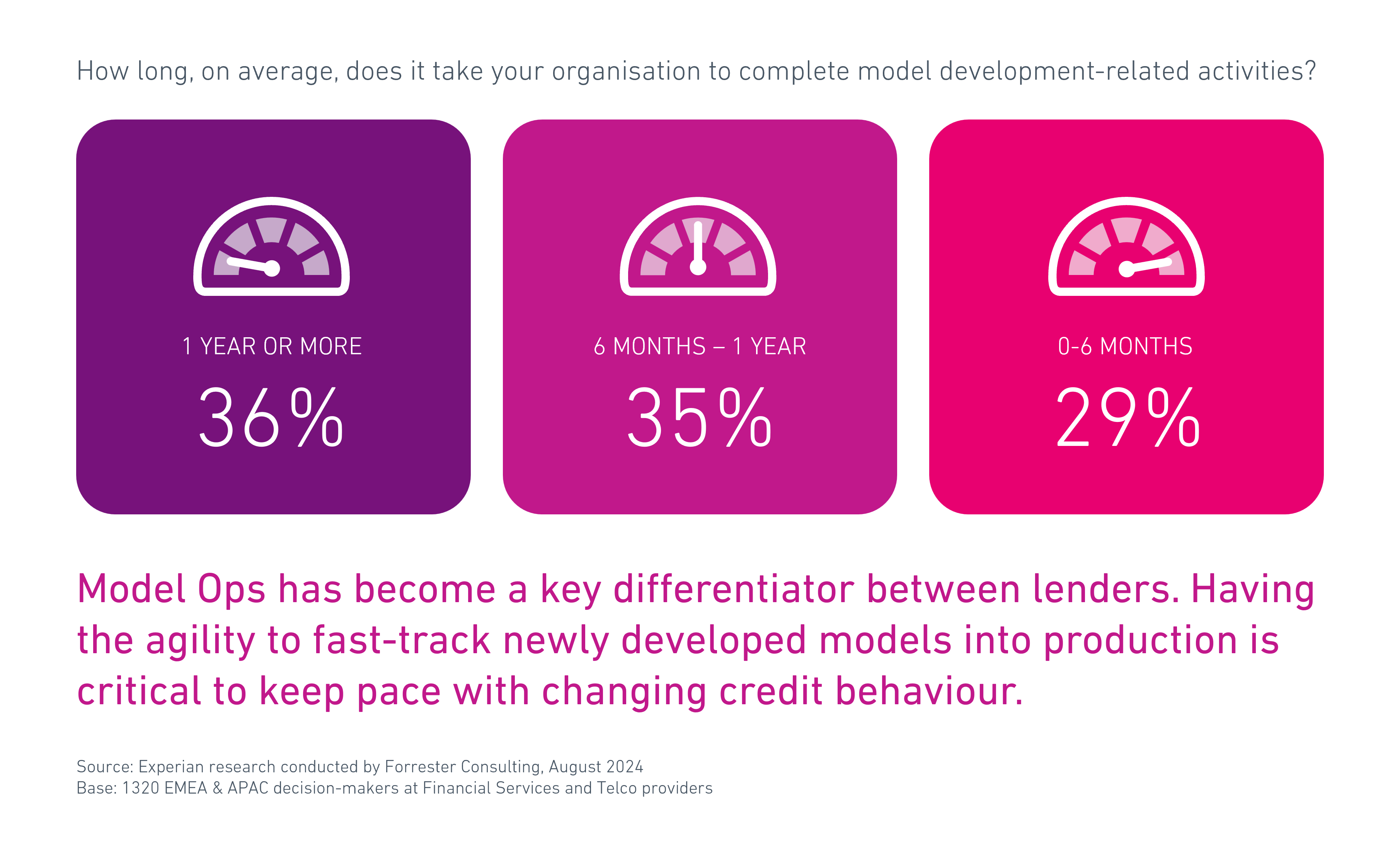

Building and deploying models shouldn’t take over a year – yet 36% of businesses do exactly that. In a landscape where credit behaviour and fraud patterns evolve quickly, slow deployment doesn’t just delay benefits; it dilutes them. Models age. Assumptions drift. When improvements are deployed late, return on investment is compromised from day one.

At the same time, 48% of organisations report updating models more frequently than ever. That means throughput – the ability to move from development to decisioning fast and safely – has become a key operational differentiator for credit and fraud leaders, data science teams, and the IT and governance functions that support them.

What’s slowing teams down?

Multi‑team collaboration – and where time is lost

When deployment activities are spread across separate systems and teams, every stage becomes sequential. Analytics teams often rely on IT to re‑code and package models before they can move into production. After this, analytics teams retest the models, taking them away from more productive work. Risk and governance functions also need to validate models for compliance and performance, adding further coordination and lapse in time. The challenge isn’t the collaboration itself – it’s the fragmented process that creates extra steps and delays.

Integration challenges

Fragmented tooling also makes it harder to move models into decisioning workflows. Deploying machine learning models through traditional processes adds another layer of complexity to integration challenges. Models frequently need to be re‑coded from their original development coding language into one recognised by the decision engine. Coupled with the non‑linear nature of model optimisation – moving back and forth between data preparation, model engineering, deployment and monitoring – this results in significant delays. The complexity increases when different databases and tools are involved.

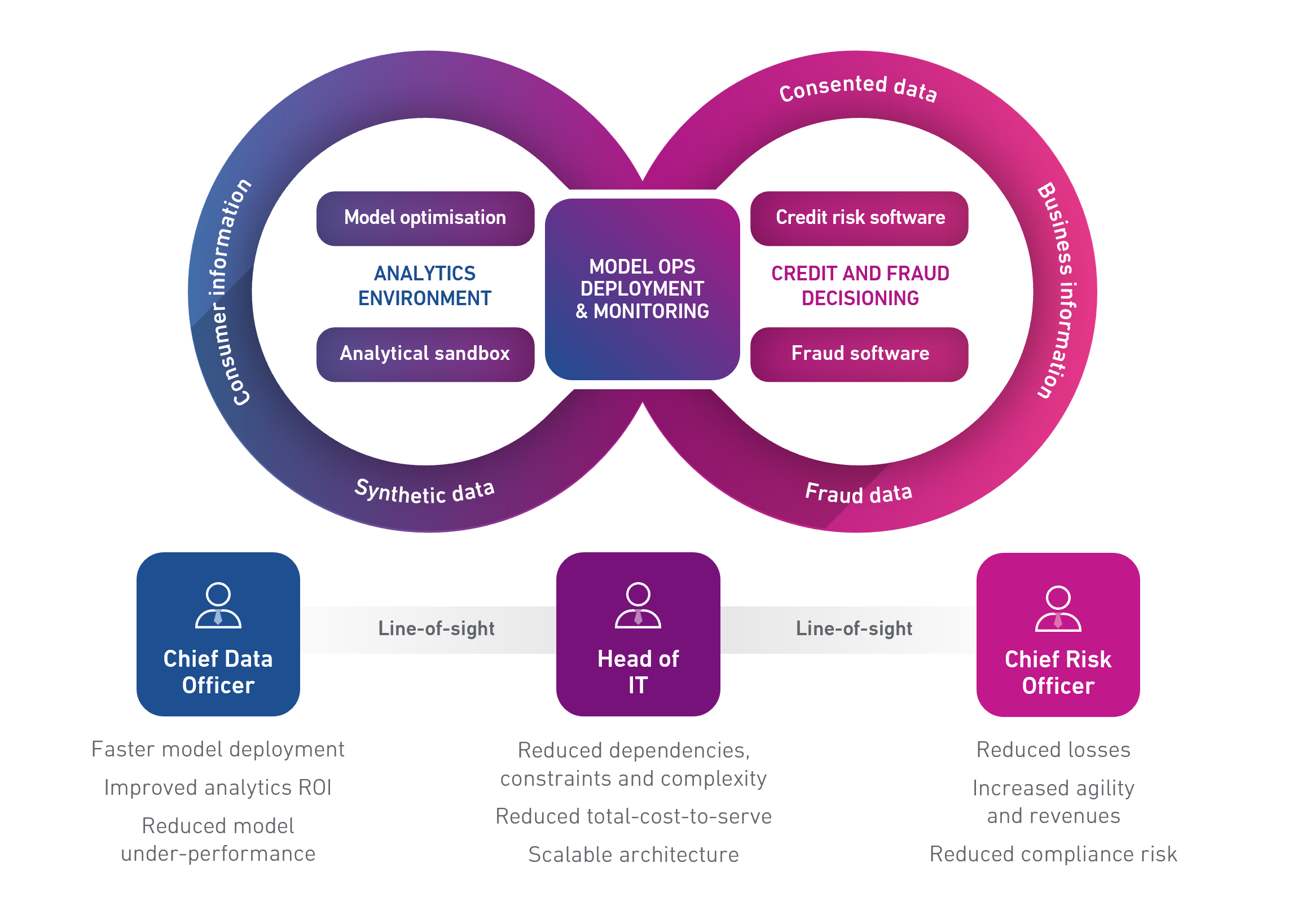

The unified answer: connecting Model Ops directly to decisioning

A unified platform connects model development, Model Ops, and decisioning software in one flow. It doesn’t remove the need for analytics, IT, risk, and governance to collaborate; rather, it reduces re-coding, tool switching, and manual packaging, and streamlines the required regression testing and compliance checks, so the same teams can move from approval to activation faster and with clearer evidence.

What changes with a unified approach:

- No re-coding: Deploy models as built, eliminating coding language translation and packaging detours.

- Auto-registration and lineage: Models carry versions, metadata, and documentation into production.

- Embedded testing: Regression, stability, and fairness checks run as part of the pipeline.

- Faster approvals: Governance is designed-in, not bolted on.

- Immediate decisioning: Approved models and their artefacts are pulled directly into decision flows.

- Continuous monitoring: Real-time metrics surface drift, bias, and performance issues with feedback to the sandbox for rapid iteration.

Until a model is live in decisioning, it represents costs, not returns. This direct connection turns the final stage from a bottleneck into a business accelerator. It’s no surprise that 54% of decision-makers believe Model Ops will be a key driver shaping the credit industry in the next 3–5 years.

Why are organisations updating their models more frequently?

- Regulatory changes, such as frameworks like IFRS 9, demand more dynamic modelling:

- Analytical modelling standards to ensure consistency, transparency, explainability and strong governance;

- Model monitoring and validation to ensure ongoing accuracy of model performance; and

- Regulatory classification and measurement of assets and liabilities (IFRS 9) to ensure standardised reporting of solvency.

- Macroeconomic factors impacting default rates and repayment behaviour.

- Implementation of advanced analytical methods like Machine Learning (ML).

- Incorporation of alternative data sources to refine predictive accuracy.

- Model development to combat emerging risks – such as climate and evolving cybersecurity threats.

The operating model – what “good” looks like

A simplified, scalable deployment process

- Build in the sandbox with your preferred tools.

- Auto-register the model with lineage, documentation, and test packs.

- Run embedded checks (regression, stability, stress, fairness/bias).

- Approve and promote via lightweight, auditable governance.

- Pull directly into decisioning – no translation or re-coding.

- Monitor in real time for performance and drift, with clear thresholds.

- Feed insights back to analytics for champion-challenger testing and rapid improvement.

Governance designed-in, not after-the-fact

- Full visibility and explainability for internal reviewers and external auditors.

- Transparent change logs and approvals to simplify model risk management.

- Continuous compliance: evidence captured automatically, not via manual collation.

Integration without friction

- Drag-and-drop decision flows across origination, account management, collections, and fraud.

- Composable components support new use cases without re-platforming.

- API-first interoperability keeps the platform open and future-proof.

Block 3 in context: a note on the full journey

Talk to an expert

© Experian, 2026. All rights reserved. The word “EXPERIAN” and the graphical device are trademarks of Experian or its related bodies corporate and may be registered in the EU, USA and other countries. The graphical device is a registered Community design in the EU. Other product and company names mentioned herein are the trademarks of their respective owners.

Disclaimer: This blog is provided by Experian Australia Pty Ltd (“Experian”) as general information and it is not (and does not contain any form of) professional, legal or financial advice. Experian and its related bodies corporate make no representations, warranties or guarantees that the information (including links and the views/opinions of authors and/or contributors) contained in this blog are error free, accurate or complete. You are solely responsible and liable for any decision made (or not made) by you in connection with the information contained in this blog. Experian (and its related bodies corporate) exclude all liability for any and all loss cost, expense, damage or claim incurred by a party as a result of or in connection with (whether directly or indirectly) this blog or any reliance on the information in this blog or links contained within. Experian owns (or has appropriate licences for) all intellectual property rights in the information and this blog must not be edited, copied, updated or republished (whether in whole or in part) in any way without Experian’s prior written consent.